DECODING THE SUBJECT

The Advanced Audit and Assurance exam is designed to reflect upon & discuss in detail the challenges faced by auditors in their professional life. You shall be required to analyze, evaluate and conclude on the assurance engagement and other audit and assurance issues in the context of best practice and current developments. AAA is generally perceived by students to be a challenging subject due to its low pass rates as compared to other ACCA papers. However, Synthesis Learning presents you with a detailed guide on tricks and tips to succeed in this paper. Explore our ACCA AAA study guide to discover effective ways to prepare for the exam.

Table Of Contents

ACCA AAA SYLLABUS

ACCA AAA PAPER PATTERN

ACCA AAA PASSING TRENDS

SOURCES OF CONTENT

STUDYING METHODOLOGY

Technical knowledge of AA

Gaining Professional Marks

Importance of SBR in AAA

THINGS TO REMEMBER WHILE WRITING THE EXAM

EXAMINER’S EXPECTATIONS

ACCA AAA SYLLABUS

The Syllabus can be broken down into the following categories:

A. Regulatory Environment

A. Regulatory Environment

A. Regulatory Environment

A. Regulatory Environment- International regulatory frameworks for audit and assurance services

- Money laundering

- Laws and regulations

B. Professional and Ethical Considerations

B. Professional and Ethical Considerations

B. Professional and Ethical Considerations- Code of Ethics for Professional Accountants

- Fraud and error

- Professional liability

C. Quality management

C. Quality management

C. Quality management- Quality management (firm and engagement level)

- Advertising, tendering, and obtaining professional work and fees

- Professional appointments

D. Planning and conducting an audit of historical financial information

D. Planning and conducting an audit of historical financial information

D. Planning and conducting an audit of historical financial information- Planning, materiality, and assessing the risk of material misstatement

- Evidence and testing considerations

- Audit procedures and obtaining evidence

- Using the work of others

- Group audits

E. Completion, review, and reporting

E. Completion, review, and reporting

E. Completion, review, and reporting

E. Completion, review, and reporting- Subsequent events and going concern

- Completion and final review

- Auditor’s reports

- Reports to those charged with governance and management

F. Other assignments

- Audit-related and assurance services

- Specific assignments

- The audit of social, environmental, and integrated reporting

- The audit of performance information (pre-determined objectives) in the public sector

- Reporting on other assignments

G. Current Issues and Developments

G. Current Issues and Developments

G. Current Issues and Developments- Professional and ethical developments

- Other current issues

H. Professional skills

H. Professional skills

H. Professional skills- Communication

- Analysis and evaluation

- Professional Scepticism and Judgement

- Commercial acumen

I. Employability and technology skills

I. Employability and technology skills

I. Employability and technology skills- Use computer technology to efficiently access and manipulate relevant information.

- Work on relevant response options, using available functions and technology, as required by the workspace.

- Navigate windows and computer screens to create and amend responses to exam requirements, using the appropriate tools

- Present data and information effectively, using the appropriate tools.

ACCA AAA PAPER PATTERN

The AAA exam is a 3-hour 15-minute assessment. The paper is divided into 2 parts: Section A and Section B.

Section A:

- Section A covers a 50 marks case study which is set at the planning stage of the audit, for a single company, a group of companies, or even several audit clients. Candidates will receive thorough information. It may differ from examination to examination but is likely to contain extracts of financial information, strategic, operational, and other relevant financial information for a client organization, as well as extracts from audit working papers, including outcomes of analytical procedures performed.

- The case study is split mainly into two parts with the first part covering risks. Here it is essential to understand the difference between the three types of risks namely business risks, audit risks, and risks of material misstatement. Separate marks are allocated towards materiality calculation and explanation.

- The second part covers topics such as ethical issues, procedures to be performed, the effect of the scenario on the report, etc.

- Out of the 50 marks, 10 marks will be allocated toward the demonstration of professional skills.

Section B:

- Section B consists of 2 case studies of 25 marks each based upon a brief situation. One question will be typically set around Section E of the syllabus (Completion, Review & Reporting), This question could be tested in a variety of styles such as evaluating the going concern status, the impact of following events, evaluating detected misstatements, and the related effect on the auditor’s report, etc. Additionally, candidates may be required to evaluate an audit report or a report that will be given to management or those in charge with governance.

- The second question of Section B can be from any other part of the syllabus with around 2 or 3 tasks/requirements.

- Each of the two case studies has 5 marks allocated towards the demonstration of professional skills.

- Other Topics such as quality management, ethics, and current issues do not have a dedicated section in which it can be expected to be tested. These topics may feature in the requirements of any 50-marker or 25-marker case studies.

Hack:

- Stick to the point: Understand the requirements section carefully. Spend some time planning your answer. Stick to the question and tailor your answer to what is asked. Note down points which you think are important to respond to the requirements. Generally, 1 mark is allocated for a well-explained point in the AAA examination.

- Do not beat around the bush: Be assertive and express each point logically. The use of the right vocabulary is very important. Master the art of detailing & yet being crisp, allowing the examiner to navigate your paper seamlessly.

- Appearing for CBE Mocks: By now, you would have realized the importance of appearing for Mock Exams in the practice platform by the ACCA. This is an absolute must to familiarize yourself with the professional-level exam environment, Appearing for 2 – 3 mocks will give you the confidence to deal with exam challenges such as speed, relevance, ability to recall & articulate, etc.

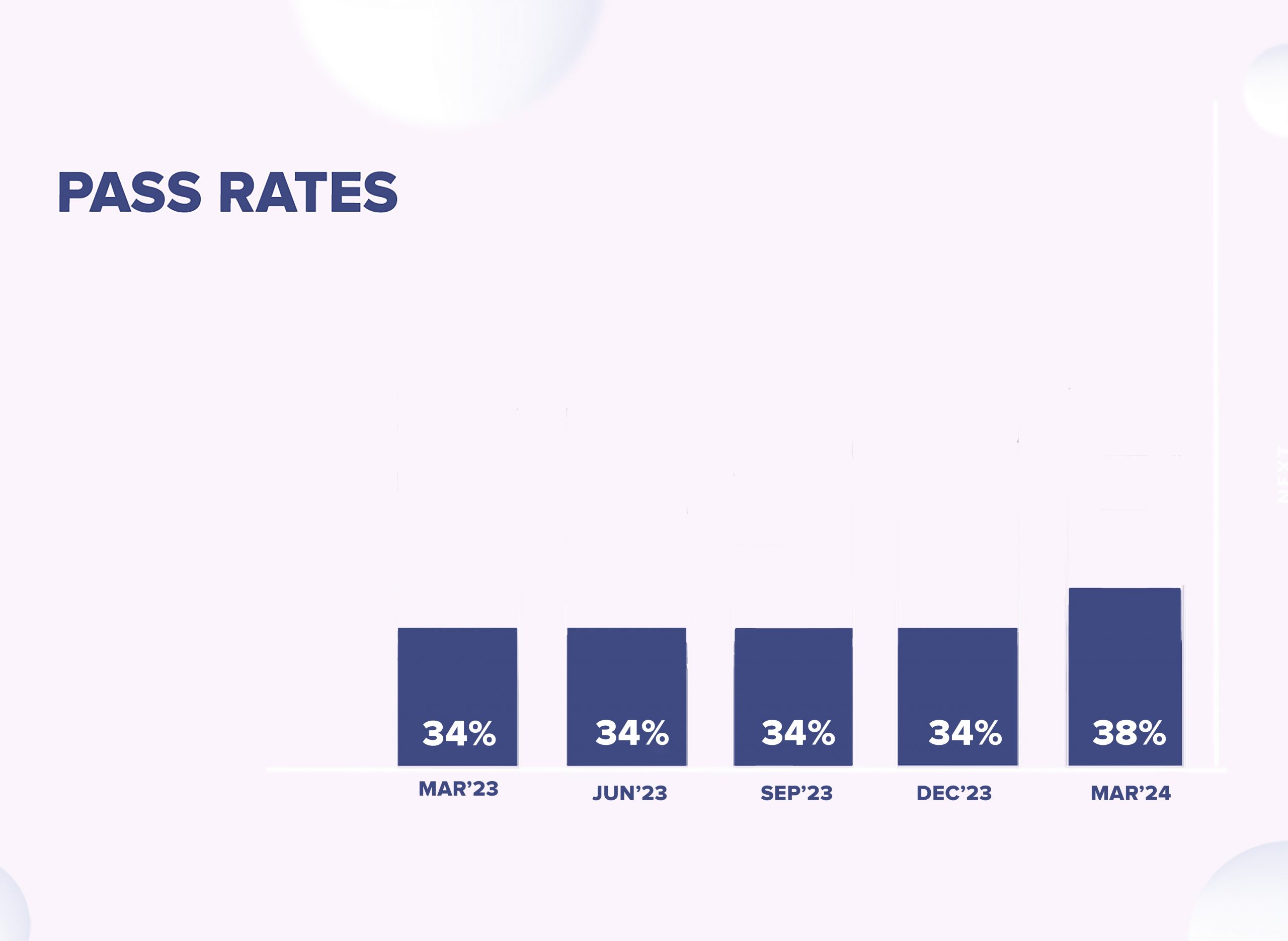

ACCA AAA PASSING TRENDS

You are expected to score 50/100 to pass this examination. This is easily manageable with a clear understanding of the concepts, good practice of the questions, and a positive attitude. The pass rates of ACCA AAA paper across the globe average between 34% – 38% for most attempts.

SOURCES OF CONTENT

You need to primarily refer to these two content sources for your preparations –

- The Study Text – for conceptual understanding

- The Practice/Exam Kit – for practice questions

There are only two ACCA-approved content providers that you should consider, namely, Kaplan Publishing and BPP Learning Media. Apart from this, you can also refer to the technical articles published by ACCA on different topics. You can use this link to refer to the articles.

Download Our Curated Express Notes For ACCA AAA Here

STUDYING METHODOLOGY

- In the first stage, master the Study Text in great detail to gain a complete understanding of the concepts & theories discussed.

- Go through the Case Studies in the Exam kit in detail. Understand the application of conceptual theories mastered in the Study Text.

- It is most advisable to solve some cases hands-on by typing them (simulating the exam environment) in the Blank Workspaces provided to you.

- Pay key attention to Examiner’s Comments to get perspective on the expectations at the examination & meet the minimum standards set by the Examining Body.

- Do not keep your studies towards the end. Ensure that you set a systematic weekly timetable & master content week after week.

Technical knowledge of AA

The core topics of AA are fundamental to the subject of advanced audit and assurance. Thus, it is assumed that candidates have knowledge of AA. These topics will continue to be examined with emphasis on the application of knowledge. AAA focuses on application, analysis, synthesis, and evaluation. Therefore, any rote learning would score little to no marks.

Gaining Professional Marks

There are 20 marks allocated to a demonstration of professional skills. These essentially judge a candidate on the display of professional and behavioral skills throughout the case requirements. These are further divided into four categories namely Communication, analysis and evaluation, professional skepticism & judgment, and Commercial acumen. Amongst the four, professional skepticism is considered to be the most important for an auditor since the auditor is expected to be independent and objective with an eye for detail towards the procedures they carry out before, during, and after the engagement. For detailed guidance on each professional mark, candidates can refer to the ACCA website.

Importance of SBR in AAA

- It is of high importance that candidates have sound knowledge of financial reporting standards and frameworks before appearing for AAA. This is especially important in the Section A question.

- Candidates must not only be able to identify the potential risks from the scenario, but they must also be able to use the financial information provided to further support their assessment of the risk through the appropriate use of analytical procedures and calculation of materiality.

- Candidates may be asked to evaluate audit risk and material misstatement risks using more complicated accounting scenarios, such as leases, share options, financial instruments, pensions, group accounting, and deferred tax accounting.

- Therefore, it is generally recommended that students appear for the SBR exam before appearing for AAA.

THINGS TO REMEMBER WHILE WRITING THE EXAM

After months of all the effort and hard work, you would’ve put into the preparation for this exam, it is equally important to ace your exam. Here are some things to remember-

- Time Management: It is important to complete the paper on time. Remember, time management is a key to success! Here is how you can allocate your time-

| AAA | |

| Section A | 1 hour 30 minutes |

| Section B | 45 minutes per case study (1 hour 30 minutes) |

| Buffer time | 15 minutes |

| TOTAL | 3 hours 15 minutes |

Be crisp and precise about what has been asked. Writing extra would not fetch you any extra marks but instead, you would lose time. Therefore, spend the allocated time wisely. Do not stress or panic over a single question during the exam, this could make other straightforward and manageable questions messed up. Try to score well on areas where you feel you have a good grip first and then return to those questions which were left at the end.

EXAMINER’S EXPECTATIONS

The ACCA publishes an Examiner’s Report for every attempt which gives an insight into the marking process, the common mistakes that students make during the exams, and other useful techniques to do well in your examination. You must go through the Examiner’s Reports to understand what the examiner is expecting from you. It will help you understand how students have failed to tackle different questions and how they could have performed better. It’s like learning from someone else’s mistakes. You can follow this link to refer to a few of the examiner’s reports published by the ACCA.